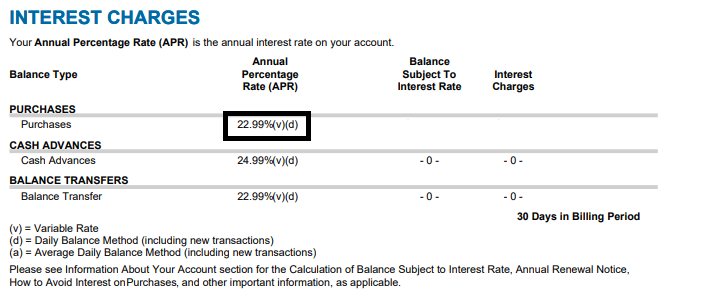

Have you ever heard the saying “A penny saved is a penny earned” (Cambridge Dictionary)? If you put money into a tax-free investment that made 22.99% and was risk free, it is the same as taking that money and paying extra to your credit card that charges 22.99% APY. Check this out:

22.99% is the interest rate I am paying on the remaining balance for this credit card. So rather than save in a .01% interest rate savings account, it would make more sense to pay extra to my credit card.

What Is Debt?

You could honestly claim debt is your mortgage, car payment, student loan payments, and or credit card payments, and you would be right. However, in my definition, debt is unsecured debt. In other words, it is debt not backed by an asset. So if you have borrowed money against your life insurance policy, that is not debt by my definition. This is simply because you would wipe out your debt with your asset.

Just like a lot of people, I have a student loan balance. I am going to separate that out because the interest rate is relatively low compared to credit card debt. But you could include this in your list of debts to pay off, it would just come after the higher interest debt.

Which Comes First, Emergency Savings Or Paying Off Debt?

First, I would find a way to stop spending on your credit cards. Yes, even before you start saving for emergencies. The whole point of having an emergency savings is to avoid accumulating debt or raiding your brokerage account, so if you are accumulating debt to save, that doesn’t work. If you have trouble with avoiding credit card use, you need to look at your budget.

Second, make sure you spend at least 20% less than you make. If you make $100, you should only spend $80. This is the goal. Look at your fixed expenses first followed by what you spend out of pocket. This may take a month or two to figure out. See if there is anything you can cut back on without significantly impacting your life.

Third, make a choice. If you truly believe you can avoid your emergency savings account, you can probably pay up to 20% of your income extra to your credit cards. But seriously, until your emergency fund is fully funded and your credit card debt is paid off, you should hold off on investing money in stocks.

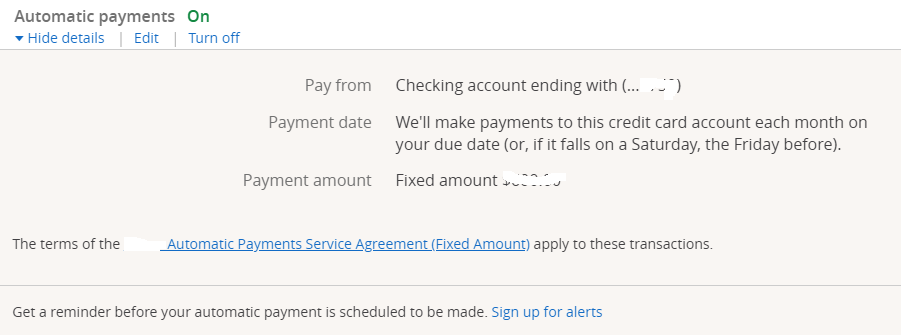

An Easy Way To Pay Extra

In my opinion, if you think too much about debt you will get more of it. You really should be thinking about the good things you will get as you progress on this journey. Instead of thinking about your debt, set up an automatic payment to pay extra:

Just make sure to enter the payments into your check book or however you keep track of your checking account (such as Quicken).

Automatic payments are like budget billing for your credit card. You set it and forget it. You just need the fixed payment to be larger than your minimum payment. And don’t forget, you are not going to spend on your credit cards. Unless you are paying them off every month of course. Credit cards should be considered a payment tool, not a way to go into debt.

Which Debts To Pay Off First?

If you have more than one unsecured debt and are wondering which debt to pay off first, wonder no more! Generally, you want to treat your debt as a savings account and tackle your highest interest rate debt first. Because you will make/save more money doing so.

Some people say to tackle your lowest balance first in order to show yourself some progress. If your interest rates are generally the same, you can do this. Otherwise, your progress will be slower overall. Just don’t worry about your debt, just pay a little extra as you would contribute to a savings account.

What If Your Unsecured Debt is 7%?

Generally, I would say that unsecured debt is bad debt. However, if you almost surely would make more money investing, you may want to just make your minimum payment for now. For instance, the S&P generally earns around 9%, so anything less than 9% could probably wait to be paid off.

You could have a different opinion and decide that you want to get rid of all of your debt, that is completely up to you.

How To Avoid Taking From Emergency Savings Or Spending On Credit Cards

Life is not always so easy. Your car breaks down. You need a new dryer. Your child needs money for a school trip. Emergencies happen all the time. Like *all the time*. Therefor, not every emergency is an emergency. In fact, almost none are.

When you encounter a challenge, instead of turning to your emergency savings or spending on a credit card, it is time to get creative. Think to yourself, “How can I get through this without using a credit card or my emergency savings?” Sometimes you can delay a payment on something. Sometimes you can spend less on something else. Sometimes you can dig up change from your cushions. Find a way. Most financial challenges do have an answer, but it’s far easier to turn to that 22.99% credit card.

More reading: